Real Estate Monthly Report, February 2022

We are going to be walking you through the most important topics in the housing market right now. We’ll be talking about homeownership as a hedge against inflation, rising mortgage rates, and the latest update that we have on forbearance.

-Roberto Montaño

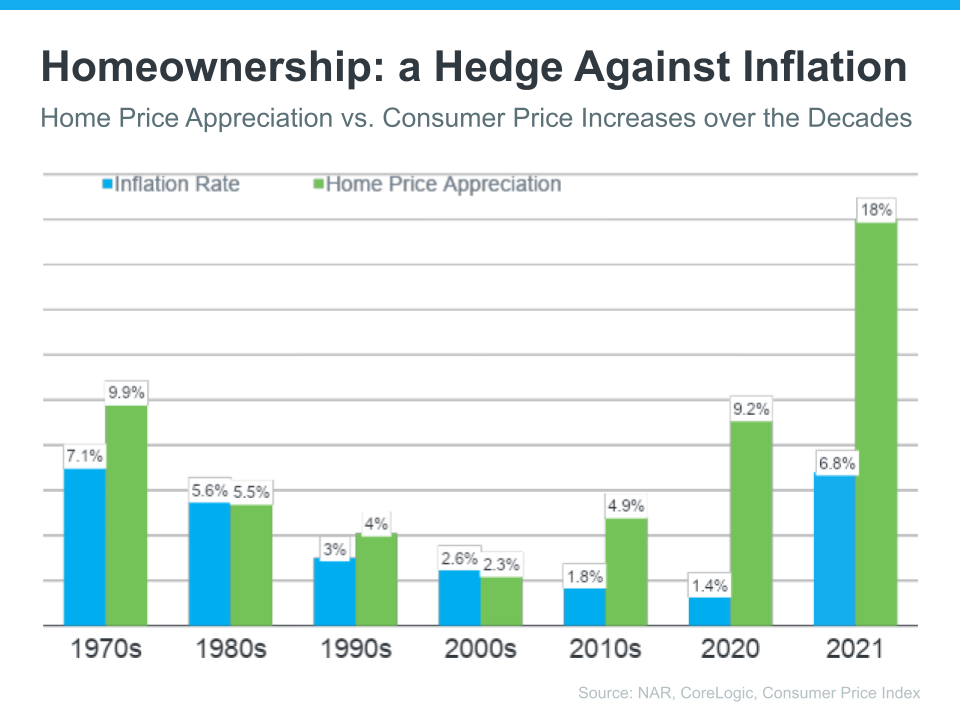

Homeownership: a Hedge Against Inflation

This is homeownership as a hedge against inflation and I want to break it down for you so you can really see what we’re talking about here. This is home price appreciation versus the consumer price increases over the decades, and it goes all the way back to the 1970s. Now what you’re looking at here is the blue bars are the average inflation rate for the decade and the green bars are the average home price appreciation for each of those decades as well. Let’s look at the 1970s to start. Inflation increased at 7.1 percent in that decade and home values appreciated at 9.9 percent in the same time period. So homeownership outperformed inflation, and where do you want to be in inflationary times? In that asset that’s outperforming inflation. Now in the 1980s it was a little bit more balance, 5.6 percent inflation, 5.5 percent home price appreciation, and look at the ‘90s. We start to see home values tick up again a little bit more, outperforming inflation throughout that decade.

Now we know the 2000s were very different. Home prices performed at a very different rate than what we’ve seen in many other decades and even what we’re seeing today and potentially tomorrow. We also had a fundamentally different housing market. We had the oversupply of homes, we had, you know lending standards that were vastly different than they are today. This is where home values really started to kick in, homes started appreciating much faster than inflation, 4.9 percent versus 1.8, and then 2020 and 2021, you know what’s happened here; massive home price appreciation, you know a drastic difference where home values outperformed inflation.

So over time what you can see is that homeownership is generally looked at as this great hedge against inflation because home values are performing better than the inflation rate. That means that someone buying a home today can lock in today’s cost and protect themselves against the rising cost of inflation in that biggest monthly payment going forward.

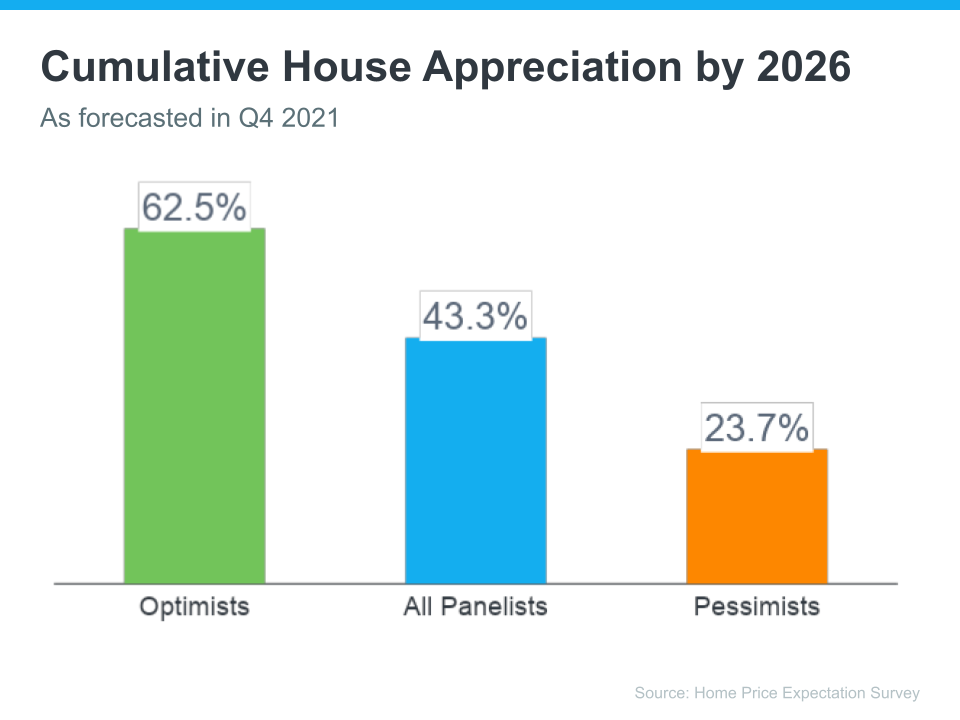

Cumulative House Appreciation by 2026

They divided out the group into optimists and pessimists, optimists being the ones projecting the most appreciation over the next appreciation over the next five years and pessimists estimating on the lower side. So take a look at that orange bar, those are the pessimists, you know the experts that are saying home price appreciation on the lower side, cumulatively, by 2026 it’s going to be over 23 percent.

So as experts look forward, the conditions of the market, what’s projected to happen? Home values are expected to increase in value over time, even on the lower end, 23 percent, 23.7 is pretty significant over the next five years, so locking in today’s cost is mission critical for those who have the opportunity to do so, to protect themselves in their largest monthly payment because as we know, with home prices rising, mortgage rates rising, inflation all around us, it’s going to get more expensive to purchase a home.

Tangible assets like real estate get more valuable over time, you’ve seen that in the graphs and the data that we’ve shown you, which makes buying a home a good way to spend your money during inflationary times.

Roberto “Beto” Montaño

Team Leader / REALTOR©

RE/MAX Partners

773-744-0238

Beto@CallBeto.com

https://CallBeto.com

5130 W. Belmont Ave. Chicago IL. 60641